Elevate the power of your work

Get a FREE consultation today!

As data center power demand continues to grow, driven by demand for cloud and AI services, grid operators in major data hubs are struggling to forecast and meet electricity needs.

As data center power demand continues to grow, driven by demand for cloud and AI services, grid operators in major data hubs are struggling to forecast and meet electricity needs.

This short Iron Mountain Data Centers (IMDC) insight paper looks at why, how and where engaging proactively and flexibly with grid operators can benefit the data center industry, support grids, and benefit all customers.

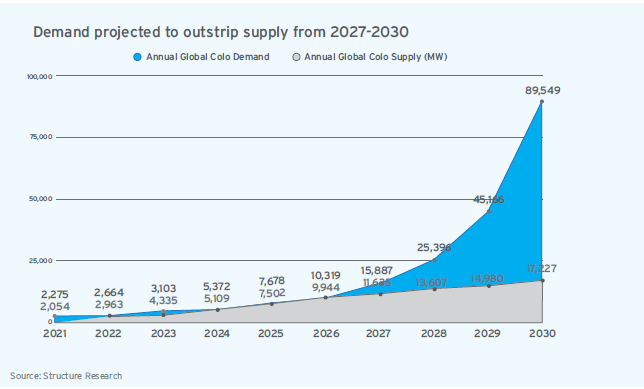

Global demand for data center capacity is projected to outstrip supply by 2027-2030, reaching nearly 90 GW by 2030. The key factor limiting the ability of the data center industry to meet this demand is power availability.

Today, data centers account for 2–4% of world power usage, with the IEA forecasting that consumption will more than double by 2030. However, in many densely developed hubs the figures are far higher. A study by Lawrence Berkeley National Laboratory stated that in 2023 America’s data centres used 176 terawatt-hours (TWh) of electricity, a figure forecast to increase to up to 580 TWh by 2028 – 12% of America’s total energy consumption.

This global phenomenon is taking place while the world’s power infrastructure is in transition. The sharp rise in power demand for AI infrastructure is taking place in parallel with the broader shift from fossil fuels to low-carbon electrification. These two trends are putting immense pressure on the transmission capacity of electricity grids, many of which were built decades ago.

Mature data hubs like Northern Virginia, Dublin, London, Singapore, Frankfurt, Amsterdam, Silicon Valley, and Phoenix are facing multi-year delays for new grid capacity, forcing developers to rethink everything from site selection to energy strategy and procurement.

Power grid operators and data center operators have very different approaches.

Predicting data center demand is challenging for grids. Due to the scale of demand for data center capacity, grid operators receive hundreds of power requests, many of which are duplicated elsewhere. The result is so-called “phantom data centers.”

These speculative requests can drive up prices. A common stipulation now from grid operators in the Northeastern U.S. is to insist on “take or pay” contracts, where utilities require substantial financial commitments in advance. This can drive up costs, and tie up large amounts of capital and credit for extended periods of time, reducing investment in certain markets and stranding capital.

Speculative power connection requests submitted simultaneously to multiple grids are creating huge numbers of “phantom data centers” which make it very hard to predict future demand accurately.

Solutions are emerging for this issue. Clear fact-based communication is essential, with partnerships emerging between power sector stakeholders, offtake (data center) operators, grid/utility operators, government and regulators. Accurate forecasting of future grid loads is critical to this effort, otherwise pricing can get out of control. Clarity, accurate planning and the avoidance of duplicated risk make for fairer contracts - for example, the Data Center Coalition, together with E3 has made a very positive contribution to a new standardized approach.

This is a first step to solving problems in collaboration with grid operators. It also establishes an important principle. Data center operators need to recognise that, unlike other more passive customers, they are in a position to help; in other words they need to be partners, not customers.

And, in addition to sharing the risk of investment in new transmission capacity, there is much more that data centers can do.

A recent survey by Bloom Energy highlighted a sudden rise in the American data center industry ́s approach to self-generated power using microgrids that take the strain off grids. The survey found that, faced with lengthening interconnection queues for grid connections, data center decision makers expect that by 2030, 38% of facilities will have at least some onsite power generation, and 27% of facilities will be 100% independently powered. This contrasts with last year’s survey, which showed 13% partially self-powered and 1% fully self-powered by 2030.

The range of self-generation options is growing. Nuclear power (e.g. Small Modular Reactors) is an increasingly popular option for large loads, but permitting, testing and commissioning the plants will take several years. Renewable investment is becoming even more aggressive and direct, with hydropower, solar and wind investments such as Google ́s $3 billion investment in hydropower in Pennsylvania, and recent purchase of Intersect Power. Onsite natural gas generation is on the rise in markets where permitting and gas pipelines allow, despite the fact that it is costly and carbon-intensive.

Where interconnection queues are very long, full Behind the Meter (BtM) builds can be completed before a grid connection becomes available, with timeframes as short as 18 months for solar and storage or natural gas. In addition to faster access to power, BtM solutions also bring greater certainty to power planning.

Leading green IT data centers with solar power, clean energy, and sustainable colocation. ESG data center solutions for corporate responsibility.

Iron Mountain's NJE-1 New Jersey data center in Edison: 830k sq ft, 30MW power, 100% renewable energy, 24/7 Smart Hands support, 20+ carriers, near NYC

Get a FREE consultation today!